When a geopolitical shock reaches the French electricity market

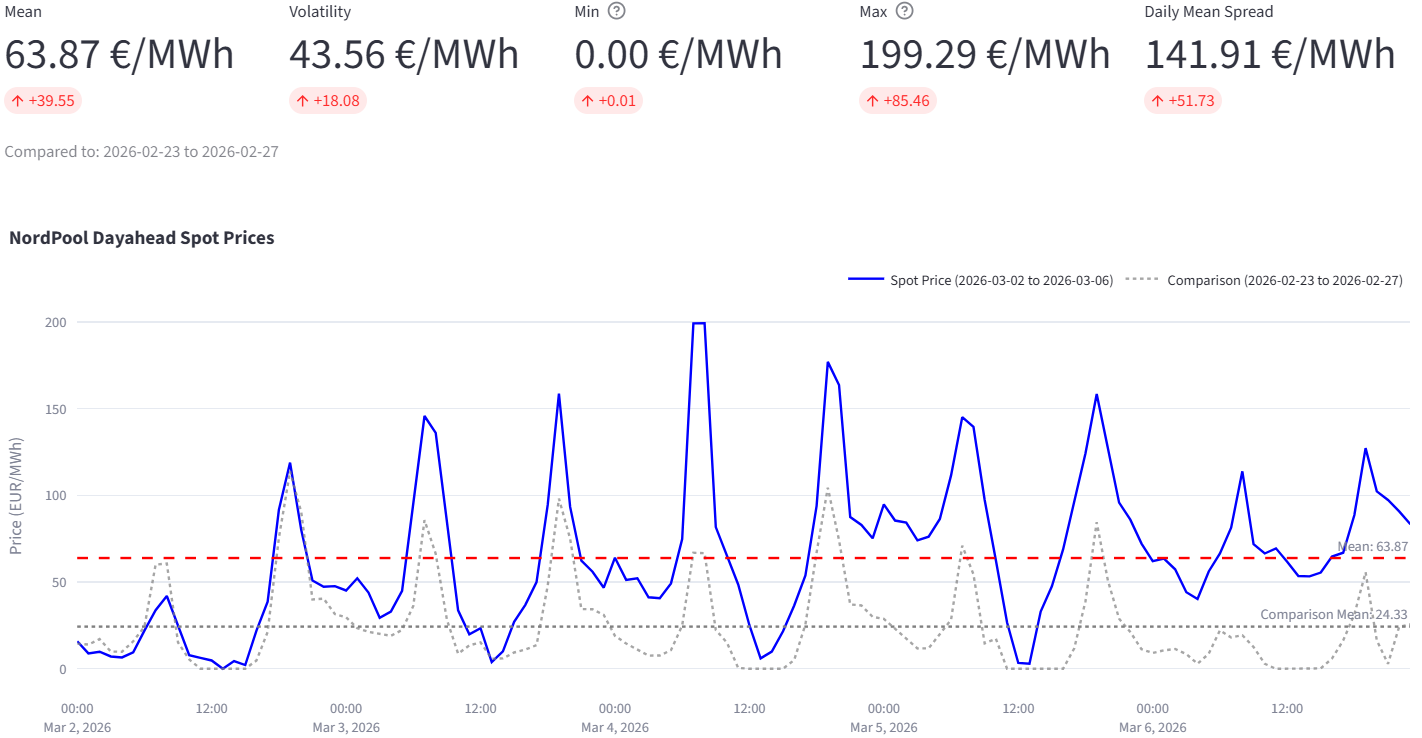

The recent increase in SPOT electricity prices in France illustrates how quickly geopolitical tensions in gas markets can spill over into the European power system. In just one week, the gas SPOT price surged by 66%, reaching €52/MWh, and this upward movement is almost mechanically transmitted to SPOT electricity prices in France. Hourly prices at times approached €200/MWh, while the dynamics of intraday spreads confirm a tighter and more volatile pricing environment. Nevertheless, weekly and monthly averages remain, at this stage, below the levels observed last year.

4 March 2026: hourly SPOT prices hits €200/MWh, intraday spread +€52/MWh

After a period marked by episodes of negative prices – a sign of a system temporarily oversupplied – the situation has reversed abruptly.

On Wednesday 4 March 2026, hourly SPOT prices nearly reached €200/MWh between 7 a.m. and 9 a.m., an increase of €95/MWh compared with the maximum observed the previous week. Over the same period, the average daily price rose by around €40/MWh, while the intraday spread (the difference between the minimum and maximum price within a day) widened by €52/MWh.

These developments reflect not only an increase in price levels but also a clear rise in intraday volatility, in a context where every supply or demand signal is amplified by tensions in the gas market.

The Math Behind €200/MWh: Breaking Down OCGT Marginal Costs

To understand why electricity prices close to €200/MWh are not “disconnected from fundamentals”, one simply needs to examine the full production cost of a gas-fired plant such as an OCGT (Open Cycle Gas Turbine).

The price levels recently observed in France are consistent with the marginal production cost of a gas-fired power plant.

Using typical assumptions for a simple-cycle gas turbine (OCGT):

around 3 MWh of gas required to produce 1 MWh of electricity,

emissions of around 630 kg of CO₂ per MWh produced,

a gas price around €52/MWh,

a CO₂ price on the EU ETS market of around €72/tCO₂.

The marginal cost calculation is therefore as follows:

Fuel cost

3 × €52/MWh = €156/MWh

CO₂ cost

0.63 × €72/tCO₂ ≈ €45/MWh

This results in a total marginal cost of around €201/MWh.

When these gas turbines are called upon to balance the electricity system, SPOT prices close to €200/MWh therefore do not reflect irrational market behaviour. Instead, they correspond directly to the translation of fuel and carbon costs into electricity prices.

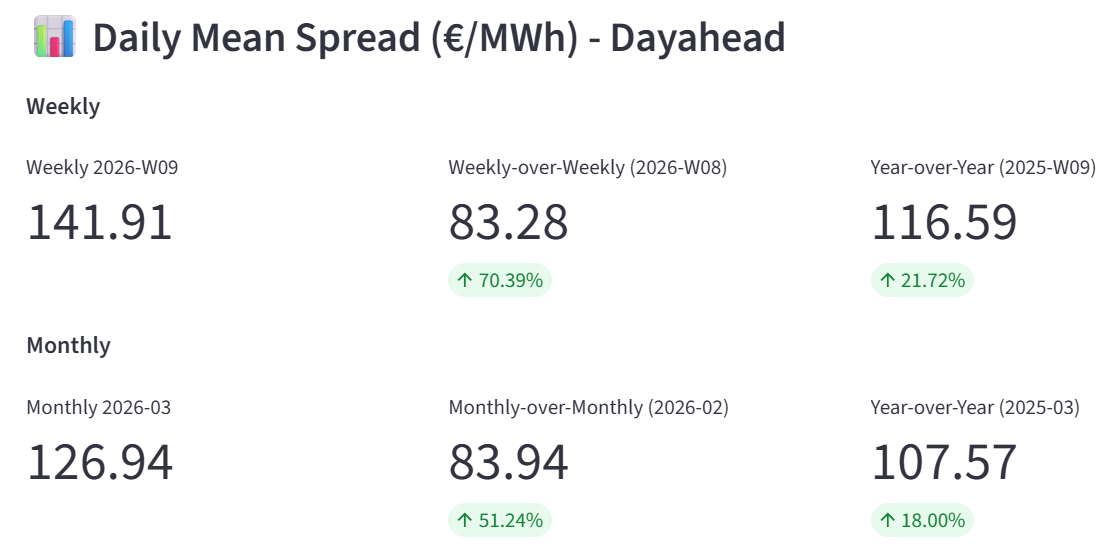

Intraday Spreads: New Opportunities for Flexible Consumers

The increase in the daily spread (+€52/MWh in one week) is another important signal.

While off-peak prices remain relatively contained, peak hours increasingly reflect the marginal cost of gas-fired generation. As a result, the gap between low and high prices within the same day is widening.

This dynamic has several implications for market participants:

For flexible consumers (industrial players, aggregators, batteries), higher spreads create greater opportunities to capture value between off-peak and peak hours.

For supply portfolios, rising volatility complicates risk management and increases the cost of hedging products.

For the electricity system, it reflects a growing reliance on expensive thermal generation during certain hours, while other periods remain relatively inexpensive.

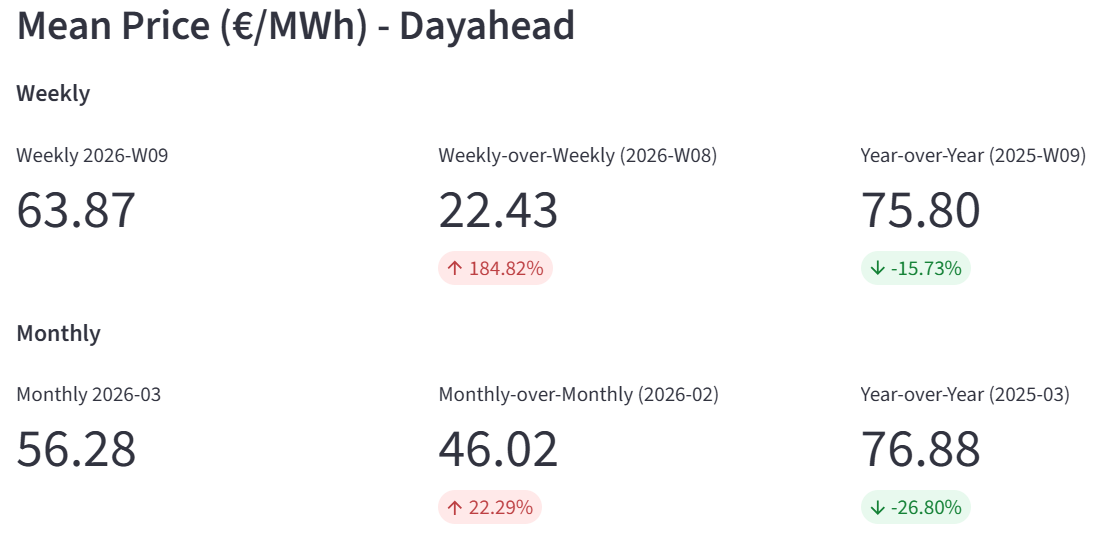

French electricity prices March 2026: still 16–27% below last year

Despite the recent spectacular increase, French SPOT prices have not yet returned to the levels observed during the same period last year:

the average weekly price remains around 16% lower,

the average monthly price is still about 27% lower.

This contrast highlights the current situation: an electricity system sensitive to geopolitical tensions, but which has not yet entered a pricing regime as persistently extreme as that experienced during the recent energy crisis.

Market Outlook: Forecasting the Next Wave of Volatility

Market developments in the coming weeks will largely depend on two main groups of factors.

The first relates to the geopolitical context and its repercussions on the gas market. The evolution of the conflict in Iran and its potential consequences for supply routes will remain a major driver of price dynamics. Any extension of tensions to other major suppliers could quickly push fuel prices higher and, in turn, raise marginal electricity generation costs across Europe.

The second concerns the fundamentals of the power system. The availability of nuclear and hydropower capacity, weather conditions, and the ability of system flexibility to absorb demand peaks will all play a decisive role in determining the scale of price movements.

In this context, market participants exposed to the SPOT market (consumers, producers, traders and aggregators) have every interest in refining their understanding of marginal costs, particularly the combined dynamics of gas and CO₂ prices. Monitoring intraday spreads is also becoming increasingly essential, as these differentials increasingly reflect the level of tension within the power system. Finally, strengthening flexibility and hedging strategies appears to be a key lever for navigating a more volatile market environment.